The Dynamics of Industrial Choice (3)

(Part 1 and 2)

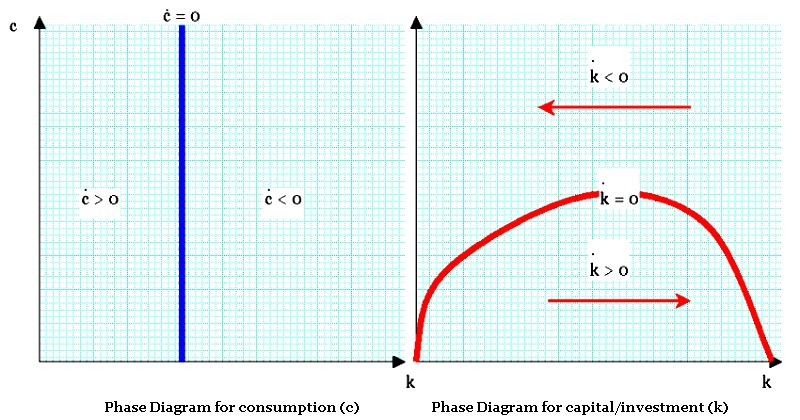

In Part 2 we had a brush with the basic classical economic growth model. The model in question has come in for a significant amount of criticism, not least because it assumes constant full employment (in the sense that unemployment is ALWAYS a choice people make), no significant effect of monopolies, and unlimited ability to defer consumption.

An issue I have with the model is that, ironically, it suppresses the truth it reveals. Technology it treats as absolutely nothing more than the disaggregated residual of economic growth, after subtracting capital and labor growth. The model mentions firms, but they have no objective function to maximize; they aren't constrained by prior technology; they aren't tied to formats. They simply provide a ratio between inputs and output; but both are homogeneous. In plain English, they assume the economy behaves like a gas, not something lumpy. Usually, when you use a mathematical model, it's simplified because there are obvious limits to the complexity of the math one may do. The model may describe optimal conditions for event x, for proving x is impossible even under the most favorable of conditions. Conversely, one might prove the inevitability of x by demonstrating that, even under the most restrictive of conditions (so restrictive they're practically impossible), x will still happen anyway. A third purpose is to show hypothetical conditions under which x could conceivably happen, even though the frequency of those conditions is subject to further inquiry. The RCK model does none of these things.

However, the RCK model can be modified to depict different things entirely. It is not very good at modeling the aggregate economy.* It is somewhat better as a conceptual tool in explaining the forces acting on actors like firms (not households). Households are too varied in character; they are too numerous; and their dynamics of maximization are incompatible with the assumptions of the RCK model. Firms can be grouped into plausible categories based on stranded costs and capital structure; in contrast, households may or may not be constrained by subsistence constraints, multiple members, perverse incentives, and unknown optimization strategies. On the other hand, firms have clear optimization goals.

Additionally, the optimality analysis for which Frank Ramsey had originally suggested his model, is a more reasonable application of the RCK model anyway. In this case, the object is to evaluate the optimality of decisions, not to make predictions or deductions of the "actually existing" economy. Such optimality information about households is, to reiterate, useless; about firms, it can be used to evaluate policy of firm administration. Corporations, with legal powers of limited liability and access to "capital markets," are, in some senses, surrogates of the state. Banks, for example, are a category of firm who are empowered to create money. Their governance is therefore a valid target of this sort of analysis.

A second modification I would recommend pertains to the objective functions that our economic agents seek to maximize. In the original RCK, if the economic actor is off the sadddle point, then it will increase savings to precisely that level required for path-convergence. Yet the functions of capital accumulation out of personal accumulation are pushing in the opposite direction; the situation can be likened to a pedestrian running frantically up a down escalator. That the escalator always points in the direction away from the equilibrium growth position, is an awkward but inevitable fact of the household savings-consumption equation; the optimization function requires that the household will [on average] react by running up the escalator faster than the escalator is moving. From experience, we know this is not true for firms, whose existence takes a clear trajectory from expansion to stagnation to financial collapse.

Corporations manufacturing a particular item are motivated to maximize earnings out of revenues. But rather than following a steady-state optimization function, they have a trajectory, or path through time. Rather than assuming the corporate management optimizes its capital structure and technology choices for a steady state growth, which is unrealistic, we would instead plot the firm as responding to conditions at any moment based on its optimization function, the capital structure, and stranded costs. Firms achieve optimization by selecting between quality and quantity (i.e., between improving processes and enlarging scale). Improved processes result in at least two positive feedbacks: higher revenues (which may persist, longer than the costs of transition to the improved process did) AND lower stranded costs (since the process is revived repeatedly, so stranded costs are reduced in the process design).

I would expect a mathematical exposition of this would reveal that, where market share is basically fixed, quality and low stranded costs would become the preferred choice; and capital structure would tend towards debt, rather than equity.

___________________________________________________

SOURCES & ADDITIONAL READING: Douglas J. Puffert, "Path Dependence, Network Form, and Technological Change" (PDF); Kenneth J. Arrow, "Path Dependence & Competitive Equilibrium" (PDF); David F. Weiman, "Building ‘Universal Service’ in the Early Bell System: The Reciprocal Development of Regional Urban Systems and Long Distance Telephone Networks" (PDF).

___________________________________________________

* That the RCK model does not describe observed reality is demonstrated by empirical comparisons of predictions of inflation, interest rates, prices of specific commodities, and so forth. A survey of the historical evidence is found in Steven M. Sheffrin's Rational Expectations. Moreover, the RCK model predicts fairly rapid rates of convergence for economies with disparate levels of productivity—provided trade barriers are low. Convergence of productivity and capital stocks among the economies of the world have not remotely matched expectations. No one has ever tweaked the RCK parameters or equations to provide reasonably accurate predictions of fluctuations of savings or capital (this has been acknowledged by the PDF files explaining the RCK model, linked in part 2.) The same is true for David Romer's Advanced Macroeconomics. Hence, the RCK does not make reasonably accurate predictions about the performance of different economies in the world.

Labels: economics, planning, Ramsey-Cass-Koopmans Model

posted by James R MacLean @ 4:49 PM

0 comments

![]()

![]()

{kind=link}

0 Comments:

Post a Comment

<< Home